Workplace Investigations

Fraud is closer than most organisations think

by Mick Symons

Employee Fraud in Australia: What Councils and SMEs Must Do to Protect Themselves in 2026

Fraud Is Closer Than Most Organisations Think

When business owners consider fraud, they often envision cybercriminals, organised crime groups, or advanced hackers operating from abroad.

The reality is often much nearer to home.

Many of the most substantial fraud losses experienced by Australian organisations involve trusted employees, managers, contractors, or suppliers. Individuals responsible often have allowed access to financial systems, procurement processes, and confidential information.

For councils and small to medium-sized enterprises (SMEs), employee fraud continues to represent one of the most significant governance and financial risks in 2026.

The impact extends significantly beyond financial loss. Fraud can severely compromise public trust, harm an organisation’s reputation, erode workplace culture, and subject leaders to increased scrutiny about their oversight responsibilities.

What Is Fraud?

Fraud occurs when an individual intentionally uses deception to secure a benefit or inflict a loss.

The benefit may encompass monetary compensation, property, contracts, services, employment opportunities, or other forms of advantage.

Fraud may occur through:

- False invoices.

- Procurement process manipulation.

- Payroll fraud.

- Expense claim fraud.

- Theft of funds.

- Misuse of company credit cards.

- False timesheets.

- Wage theft.

- Cyber-enabled financial fraud.

The Association of Certified Fraud Examiners consistently estimates that organisations incur losses of about five % of their annual revenue because of fraud. For many SMEs, that level of loss can be financially devastating.

What Motivates Employees to Commit Fraud?

One of the most widely recognised explanations continues to be the Fraud Triangle.

The model shows that fraud arises when three elements converge:

Pressure

Employees may encounter financial difficulties, gambling challenges, addiction concerns, familial pressures, or substantial personal indebtedness.

Amid ongoing cost-of-living pressures across Australia, financial stress is contributing to an increased risk of fraud.

Opportunity

Opportunity often entails the highest level of risk.

Employees engage in fraudulent activities when they perceive vulnerabilities in internal controls and believe such actions will go undetected.

Inadequate procurement controls, insufficient segregation of duties, excessive reliance on trust, and limited oversight often create conditions conducive to fraud.

Rationalisation

Offenders often justify their conduct.

Typical rationalisations include:

- “I deserve it.”

- “I’m only borrowing the money.”

- “The organisation owes me.”

- “Nobody will notice.”

Many fraudsters initially engage with relatively small amounts before progressively escalating their activities.

The Fraud Triangle has evolved into the Fraud Diamond, with a fourth element representing the offender’s capability to manipulate the system and commit fraud.

Recent Australian Examples

Recent cases illustrate how trusted employees can be responsible for substantial losses.

In 2026, a former finance executive pleaded guilty to gaining nearly $500,000 from his employer through over 100 unauthorized financial transactions. The offence took place during his tenure in a trusted senior finance position. (Herald Sun)

In a separate matter, a Cronulla RSL employee has been charged in connection with allegations of fraudulent transactions exceeding $367,000. The club then reported potential losses totalling about $1.46 million over a two-year period. The purported misconduct was identified internally before being referred to law enforcement. (News.com.au)

Both matters highlight a consistent theme: fraud often arises when trusted employees have access to systems and funds with limited oversight.

Warning Signs Organisations Should Never Ignore

Fraud investigations often uncover indicators that were present well before the fraud was identified.

Typical indicators include:

- Employees declining to take leave.

- Hesitancy to delegate responsibilities.

- Excessive oversight of financial processes.

- Records are missing.

- Unusual supplier relationships.

- Sudden unexplained wealth.

- Consistent circumvention of established approval procedures.

- Bullying behaviour that inhibits critical examination.

- Notable shifts in purchasing patterns.

Trust is important.

Trust without verification introduces risk.

Emerging Fraud Risks in 2026

Fraud has undergone significant evolution.

Organisations are increasingly facing:

- Business email compromise fraud schemes.

- Fake supplier invoices.

- Payroll diversion fraud schemes.

- Collusion in procurement.

- Electronic record manipulation.

- Fraudulent vendor arrangements.

- Cyber-enabled theft.

As of 1 January 2025, the intentional underpayment of employees has been classified as a criminal offence under Commonwealth law. Organisations must now address wage theft within their fraud and compliance frameworks. (Fair Work Ombudsman)

How Councils and SMEs Can Prevent Fraud

Effective fraud prevention requires a systematic and structured approach.

Strengthen Governance

Leaders must actively oversee procurement processes, financial controls, and delegated authority arrangements.

Segregate Duties

No individual employee should have sole responsibility for managing an entire financial process from start to finish.

Conduct Regular Audits

Routine and surprise audits often detect issues before losses intensify.

Manage Conflicts of Interest

Undisclosed conflicts continue to represent one of the most common sources of procurement fraud and misconduct.

Train Employees

Fraud awareness training enables staff to recognise potential risks and understand their reporting responsibilities.

Support Whistleblowers

A significant number of fraud cases are identified through employee tip-offs rather than audits.

Employees should be assured that they can report concerns without fear of retaliation.

Final Thoughts

Organisations most at risk are often those that assume fraud could never affect them.

Regrettably, many fraud investigations begin with precisely that assumption.

For councils and SMEs, fraud prevention extends beyond merely fulfilling compliance requirements. It is a fundamental governance responsibility.

Strong controls, careful oversight, ethical leadership, and a culture that promotes transparent reporting continue to represent the most effective defences against employee fraud.

Fraud cases seldom raise whether warning signs were present.

The key question is whether any action was taken upon their initial appearance.

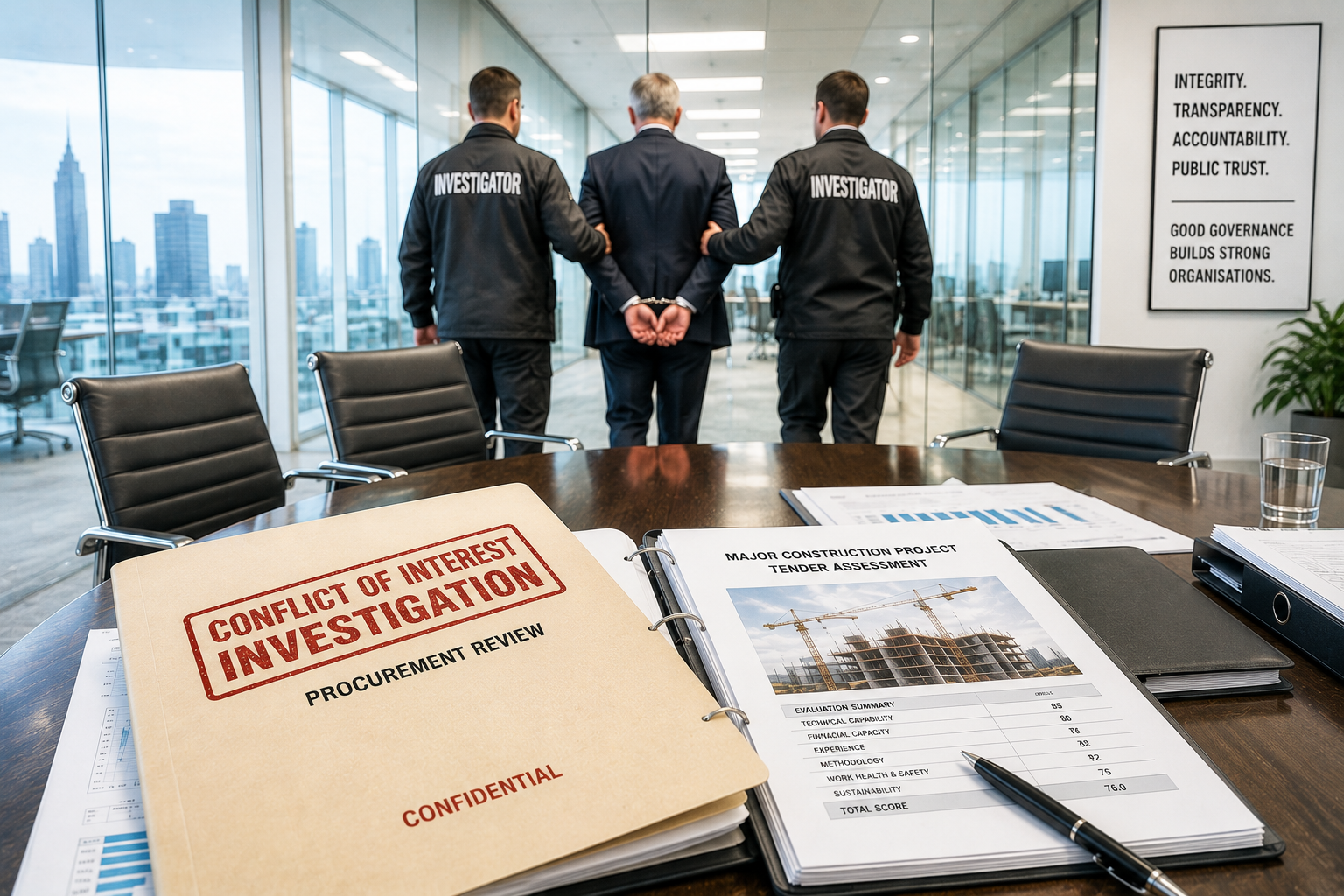

The Pyramid of Corruption: Why Small Ethical Breaches Become Major Scandals

by Mick Symons

The Pyramid of Corruption: Why Small Ethical Breaches Become Major Scandals

What Councils and SMEs Need to Know in 2026

When considering corruption, most individuals typically envision large-scale fraud, bribery, criminal prosecutions, or prominent media scandals.

The reality is vastly different.

Significant corruption cases seldom originate with a suitcase of cash or a multi-million-dollar fraud. They often begin with minor ethical compromises that go unchallenged. A favour granted to a colleague. A conflict of interest that has not been disclosed. A gift accepted without hesitation. A procurement shortcut that may seem initially inconsequential.

These seemingly minor breaches are the foundation of what is commonly called the Pyramid of Corruption.

For councils, government agencies, and small to medium-sized enterprises (SMEs), a thorough understanding of this idea is essential. Organizations that disregard low-level misconduct often establish conditions conducive to serious fraud, corruption, governance failures, and reputational damage.

Understanding the Pyramid of Corruption

The Pyramid of Corruption shows how misconduct intensifies in the absence of timely organizational intervention.

At the foundation of the pyramid lie minor ethical breaches. As these behaviours become normalised, more serious misconduct usually arises. Over time, corruption becomes ingrained in the organization’s culture.

By the time organizations recognise the issue, the financial, legal, and reputational consequences may be large.

The principle is clear: preventing corruption begins well before the involvement of fraud investigators.

The Foundation: Small Ethical Breaches

Most corruption scandals originate from conduct that employees and managers often regard as inconsequential.

Typical examples include:

- Undisclosed conflicts of interest.

- Acceptance of gifts and benefits.

- Favouritism in recruitment decisions.

- Misuse of vehicles, equipment, or resources.

- Manipulation of leave records or timesheets.

- Circumventing procurement procedures.

- Failure to declare secondary employment.

Individually, these actions may seem insignificant. Together, they foster a culture in which employees perceive rules as flexible and accountability as unlikely.

Once that mindset is established, the organization becomes susceptible to more serious misconduct.

A recurring observation by anti-corruption agencies throughout Australia is that misconduct often arises not from the absence of policies, but from their disregard or inconsistent enforcement. The NSW ICAC has consistently identified procurement environments in which gifts, benefits, and supplier relationships have influenced decision-making, despite formal policies and controls.

The Middle Layer: Fraud and Abuse of Authority

As ethical standards decline, the potential for fraud and abuse correspondingly rises.

This stage typically involves:

- Procurement related fraud.

- Tender process manipulation.

- Incorrect invoicing.

- Improper use of organizational funds.

- Unauthorized expenditure.

- Improper exercise of delegated authority.

- Giving preferential treatment to suppliers or contractors.

For councils, procurement continues to represent one area with the highest risk of corruption.

The NSW Independent Commission Against Corruption has extensively investigated council procurement processes, identifying instances where employees manipulated purchasing decisions, showed preferential treatment to suppliers, or accepted benefits for awarding contracts.

SMEs face similar risks. Many business owners place considerable trust in long-tenured employees while exercising limited financial oversight. Regrettably, trust without verification may give rise to opportunities for misconduct.

The Queensland Crime and Corruption Commission’s 2025 analysis of local government corruption risks identified procurement activities, rising infrastructure spending, and evolving operating environments as critical areas requiring enhanced governance oversight.

The Top of the Pyramid: Systemic Corruption

At the highest level, corruption is integrated into the organizational culture.

Employees no longer perceive misconduct as an isolated occurrence. So it is regarded as “how things are done around here..”

Warning signs include:

- Widespread conflicts of interest.

- Collusion between employees and suppliers.

- Manipulated procurement outcomes.

- Suppression of complaints.

- Retaliation against whistleblowers.

- Lack of executive action despite acknowledged concerns.

- Systematic concealment of improper conduct.

When corruption reaches this stage, organizations often encounter regulatory investigations, media scrutiny, and substantial reputational harm.

Restoring public trust may require several years.

A Recent Example: Governance Failures Under Investigation

Recent developments illustrate how governance issues may intensify in the absence of adequate oversight.

In June 2026, the NSW Independent Commission Against Corruption ICAC) started public hearings relating to the University of Wollongong, addressing allegations related to recruitment practices, conflicts of interest, and contract awards. The inquiry is examining whether senior officials manipulated recruitment processes and whether contracts were awarded without governance and due process.

The inquiry is assessing whether senior officials influenced recruitment processes improperly and whether contracts were awarded absent governance and due process. Instead, they focus on governance controls, conflicts of interest, decision-making processes, and accountability.

This reflects an increasing trend throughout Australia. Integrity agencies are placing increasing emphasis on governance deficiencies that create opportunities for misconduct before financial losses.

The key takeaway for councils and SMEs is clear: inadequate governance often serves as the conduit through which corruption risks arise.

The Hidden Enablers of Corruption

Corruption seldom thrives in isolation.

Organizational deficiencies often contribute to the escalation of misconduct.

Poor Leadership

Employees observe leaders’ actions significantly more attentively than their words.

If leaders disregard misconduct, neglect to address complaints, or enforce standards inconsistently, employees promptly perceive that integrity is discretionary.

Policies That Exist Only on Paper

Many organizations have excellent policies.

Far fewer have effective implementation.

A code of conduct that remains unread on an intranet will not effectively prevent corruption.

Employees require practical guidance, consistent reinforcement, and transparent accountability.

Inadequate Training

Many employees receive minimal training on:

- Potential Conflicts of Interest.

- Procurement Integrity.

- Fraud awareness.

- Gifts and benefits.

- Reporting Responsibilities.

Without education, employees rarely identify risks before issues arise.

Fear of Speaking Up

A key indicator of corruption is an organizational environment in which employees feel apprehensive about reporting concerns.

Recent governance reforms throughout Australia have further enhanced protections for whistleblowers, recognising that reporting remains one of the most effective means of early misconduct detection. In June 2026, the Alice Springs Town Council implemented an enhanced whistleblower policy aimed at safeguarding individuals who report misconduct and protecting them from retaliation.

How Councils and SMEs Can Break the Pyramid

The most effective corruption prevention strategies prioritise addressing misconduct at the foundational level to prevent its escalation.

Build an Ethical Culture

Integrity must be integrated into daily decision-making processes.

Employees should recognise that ethical conduct is a compliance obligation and a fundamental organizational value.

Strengthen Procurement Controls

Procurement continues to be among the highest risk functions within both councils and SMEs.

Regular reviews ought to assess:

- Tendering procedures.

- Delegations.

- Vendor Partnerships.

- Contract variations.

- Conflict of Interest Disclosures.

Establish Effective Reporting Channels

Employees must know:

- Procedures for Reporting Concerns.

- Intended Recipients of Reports.

- What protections exist.

- Next steps following the submission of a report.

Confidence in reporting systems substantially enhances the accuracy of early detection.

Conduct Regular Audits

Routine audits should concentrate on:

- Financial control measures.

- Procurement Operations.

- Delegated authority.

- Recruitment Procedures.

- Conflict management frameworks.

Audits often detect emerging risks before their escalation into significant issues.

Investigate Concerns Promptly

Minor misconduct issues should never be disregarded simply because they seem insignificant.

Timely intervention often mitigates the need for more extensive and costly investigations.

Final Thoughts

The Pyramid of Corruption serves as a compelling reminder that significant integrity failures seldom occur abruptly.

Most corruption scandals originate from minor ethical compromises that are overlooked, justified, or normalised.

For councils and SMEs, the challenge extends beyond merely identifying major instances of corruption. The challenge lies in identifying and addressing the behaviours at the base of the pyramid before they escalate into more serious issues.

Effective governance, competent leadership, robust reporting systems, and proactive investigations continue to be the most effective tools for preventing corruption.

Organizations that take early action safeguard not only their financial assets but also their reputation, organizational culture, and public trust.

In 2026 and the future, integrity will be recognised as more than merely a compliance issue. It is a strategic business priority.

Contact ACCA ([email protected]) for help in this area.

Is Legal privilege still relevant in workplace investigations

by Mick Symons

https://youtu.be/XVhcrq9W72M

Can a Brief Touch Still Lead to Dismissal in Australia in 2026?

by Mick Symons

Can a Brief Touch Still Lead to Dismissal in Australia in 2026?

Many employees still believe that a brief physical interaction at work — a touch on the back, shoulder, waist or even buttocks — is unlikely to justify dismissal.

That assumption is increasingly risky.

Australian workplaces in 2026 operate under far stricter expectations concerning workplace behaviour, sexual harassment and psychological safety. Employers now face significant legal obligations to prevent inappropriate conduct, and tribunals are applying modern community standards when assessing workplace misconduct.

One Fair Work Commission decision that continues to influence employers and investigators is John Keron v Westpac Banking Corporation [2022] FWC 221. (DWF)

The decision sends a clear message:

Even a brief intentional touch can justify dismissal if it breaches workplace standards and undermines workplace safety and respect.

The attached draft article provided an excellent foundation for this discussion.

The Westpac Decision Still Matters in 2026

The case involved a senior Westpac manager with more than 35 years of otherwise unblemished service. After a compulsory professional development workshop, employees attended a work-related social gathering at a hotel venue.

Later in the evening, CCTV captured the employee placing his hand on a female colleague’s lower buttocks and moving it upwards toward her waist. Westpac conducted an internal investigation and terminated his employment for serious misconduct. The employee then challenged the dismissal in the Fair Work Commission.

Deputy President Binet upheld the dismissal. (DWF)

Importantly, the Commission acknowledged that community expectations regarding consent and workplace conduct had significantly changed.

The Commission stated:

“The bar as to what constitutes consent for physical and sexual interactions has been significantly raised in the broader community.” (DWF)

That observation remains highly relevant in 2026.

“It Was Only a Joke” No Longer Provides Protection

Historically, some workplace behaviour was minimised as “banter”, “harmless fun” or “nothing serious”.

Australian employers can no longer afford to adopt that approach.

The introduction of positive duties under anti-discrimination legislation, increased psychosocial safety obligations under work health and safety laws, and heightened public awareness following national workplace harassment inquiries have fundamentally shifted employer expectations.

Today, employers must actively prevent inappropriate conduct, not merely respond after the damage occurs.

That includes:

- unwanted touching;

- sexually suggestive conduct;

- inappropriate jokes;

- physical familiarity;

- after-hours misconduct connected to work; and

- behaviour occurring at conferences, Christmas parties or networking events.

The key issue is not whether the employee intended harm.

The key question is whether the conduct was unwelcome and whether it breached workplace standards.

Work Functions Are Still Workplaces

One of the most important aspects of the Keron decision involved the Commission’s finding that the conduct remained sufficiently connected to employment even though it occurred after formal work activities had ended. (DWF)

Many employees wrongly assume workplace rules stop applying once alcohol is served or official hours finish.

They do not.

In 2026, employers routinely investigate conduct occurring at:

- Christmas functions;

- conferences;

- interstate travel;

- training programs;

- networking events;

- client dinners;

- sporting events; and

- informal after-work drinks.

If there is a sufficient connection to employment, disciplinary action may follow.

The Fair Work Commission has repeatedly confirmed that out-of-hours conduct may justify dismissal where the behaviour damages workplace relationships, creates safety risks or harms the employer’s reputation. (Holding Redlich)

Alcohol Is Not an Excuse

Alcohol continues to play a major role in workplace misconduct investigations.

However, intoxication rarely excuses inappropriate conduct.

In Keron, the Commission accepted the employee had consumed substantial alcohol but still concluded the conduct justified dismissal. (Holding Redlich)

In fact, intoxication may increase employer concerns because impaired judgment can heighten workplace safety and reputational risks.

Employers now regularly remind staff that workplace behaviour expectations continue to apply regardless of alcohol consumption.

Training and Policies Matter

Another critical issue in the Westpac matter involved workplace training.

The Commission noted that Westpac had provided training concerning sexual harassment, discrimination and workplace conduct shortly before the incident occurred. (DWF)

That significantly strengthened Westpac’s position.

The lesson for employers is clear.

Policies sitting unread on an intranet will not adequately protect an organisation.

Training must be:

- regular;

- practical;

- contemporary;

- scenario-based; and

- actively reinforced by management.

Employees should clearly understand:

- what constitutes inappropriate conduct;

- how workplace standards apply at social events;

- the consequences of misconduct; and

- how complaints will be investigated.

This issue is particularly important for councils, government agencies and SMEs where informal workplace cultures sometimes blur professional boundaries.

Procedural Fairness Still Matters

Importantly, stronger expectations around workplace conduct do not remove the obligation for procedural fairness.

Employers must still conduct proper investigations before making disciplinary decisions.

A fair investigation should assess:

- witness evidence;

- CCTV or electronic evidence;

- surrounding circumstances;

- workplace policies;

- credibility issues; and

- whether the alleged conduct actually occurred.

Australian tribunals continue to criticise employers who rush investigations or predetermine outcomes.

Even where allegations involve sensitive conduct, employers must ensure investigations remain impartial, balanced and evidence-based.

The 2026 Reality

The modern workplace has changed.

Conduct once dismissed as “minor” can now result in serious disciplinary action, including termination of employment.

Employees should understand that brief physical contact may still breach workplace policies, particularly where the conduct is intimate, unwelcome or capable of causing discomfort.

For employers, the message is equally clear:

Strong workplace culture requires more than policies alone. It requires leadership, training, consistent enforcement and professionally conducted investigations.

Failing to act appropriately may expose organisations to:

- unfair dismissal claims;

- sexual harassment complaints;

- workers compensation claims;

- psychosocial hazard investigations;

- reputational damage; and

- regulatory scrutiny.

In 2026, Australian workplaces are expected to be respectful, psychologically safe and professionally managed.

Tribunals are making it increasingly clear that employers who enforce those standards reasonably and fairly will often receive strong legal support from the Fair Work Commission. (DWF)

Is Legal Professional Privilege Still Relevant for Workplace Investigations in 2026? Updated article

by Mick Symons

Is Legal Professional Privilege Still Relevant for Workplace Investigations in 2026?

Updated for 2026: New Case Law and Practical Lessons

This article has been updated to include recent Federal Court commentary, Fair Work Commission decisions and practical guidance for councils, government agencies and SMEs conducting workplace investigations where legal professional privilege may be in issue. Original article can be read here

Many councils, government agencies, and employers still believe that hiring lawyers to carry out a workplace investigation automatically protects the process with legal professional privilege.

That idea is still risky.

Australian courts and tribunals keep confirming that simply having a law firm involved does not create privilege. The crucial question is whether the investigation is mainly to get legal advice or to get ready for a lawsuit.

By 2026, this problem has become more important because investigations now more often include:

- psychological and social risks

- accusations of bullying and harassment

- complaints about unwanted sexual behaviour

- reporting of wrongdoing by an insider

- code of Conduct breaches

- conflicts of interest

- fraud and corruption allegations

- unfair dismissal proceedings; and

- workers’ compensation and workplace conflicts

Employers who do not understand privilege may accidentally reveal sensitive information during lawsuits, Commission hearings, court reviews, and investigations.

The Key Legal Principle

The High Court’s decision in Esso Australia Resources Ltd v Commissioner of Taxation (1999) 201 CLR 49 is still the fundamental rule. Privilege applies only when the main reason for the communication or document is to get or give legal advice, or to use it in current or expected legal cases.

Who the investigator is does not matter.

If the primary goal of the investigation is to find out if rules were broken, if bad behaviour happened, or if someone should be disciplined, then privilege might not protect the information.

The Fair Work Commission Warning Employers Still Ignore

One of the most important workplace investigation decisions is Gaynor King [2018] FWC 6006.

The City of Darwin hired Minter Ellison to look into bullying claims. The Council later said the report was confidential because lawyers carried out the investigation.

Commissioner Wilson did not accept that argument.

The Commission looked into the real reason for the investigation and found that the main goal was to see if workplace behaviour rules and Council policies were broken, not to get legal advice.

The Commission also looked at how the employer acted: employees were told about the investigation, the accusations, and the results. Sharing this information weakened the claim of privilege.

That decision is still very important in 2026 because many organisations still organise investigations in ways that do not protect privilege.

Why Some Investigation Reports Remain Protected

Privilege applies when the investigation is done mainly to get legal advice.

In the cases Bowker, Coombe and Zwarts v DP World Melbourne Ltd [2015] FWC 7312 and Kirkman v DP World Melbourne Ltd [2016] FWC 605, the Fair Work Commission agreed that certain information was protected because the investigators were hired specifically to help lawyers give legal advice.

The Commission examined:

- the exact words used in the retainer

- the role of the lawyers

- the reason for the investigation

- how documents were managed

- whether findings were broadly disclosed; and

- whether the employer kept things confidential as they should

Privilege is determined by how things are organised, their goals, and how people behave—not by job titles or guesses.

Recent Federal Court Commentary (2023–2026)

The Federal Court’s decision in Diawara v National Australia Bank Limited [2023] FCA 1048 provides one of the most important recent clarifications. (Australasian Lawyer)

The case was about a claim of privilege over a cultural review report created during a discrimination dispute. The Court confirmed that:

- the dominant purpose test remains the central inquiry

- the focus is on why the person made or obtained the document

- the party claiming privilege must prove the necessary facts; and

- privilege can apply even if the document is used for secondary or additional purposes

The Court looked at the agreement between Herbert Smith Freehills and Wise Workplace Solutions and agreed that the main reason for the report was to help the lawyers legally advise NAB.

This decision confirms that privilege can be kept, but only when the evidence clearly shows that the main reason was legal advice.

Recent Oversight Commentary

A 2022 external review by the South Australian Ombudsman highlighted the importance of the dominant purpose test when evaluating claims of privilege over investigation materials. The Ombudsman said that if investigations mainly focus on gathering facts about employee complaints or policy violations, claims of privilege might fail unless the evidence clearly shows the investigation was for obtaining legal advice.

The Ombudsman also emphasised that labelling a document “privileged and confidential” does not make it privileged. Courts and oversight agencies will focus on the true nature of the work and the actual reason for the investigation.

Why This Matters for Local Government

The problem is especially serious for councils.

Local government investigations often include:

- councillor behaviour

- allegations against a senior executive

- code of Conduct matters

- complaints about bullying

- procurement concerns

- allegations of corruption

- protected disclosures; and

- conflicts of interest

Many councils believe that hiring outside lawyers guarantees privacy.

That assumption becomes a problem when things get to:

- The Fair Work Commission

- NCAT

- ICAC

- The NSW Ombudsman

- Legal process

- Public interest disclosure investigations; or

- Judicial review.

If privilege doesn’t apply, sensitive information might be exposed, including:

- draft findings;

- internal communications;

- witness credibility assessments;

- legal assumptions;

- procedural weaknesses; and

- governance failures.

The Practical Lessons for Employers in 2026

Organisations should not automatically assume they have special rights just because lawyers are investigating.

The safer approach is to separate:

- factual investigations

- disciplinary decision-making

- witness evidence collection; and

- legal advice.

Employers should get advice early on how to organise the investigation before choosing investigators.

- Retainer documents are important.

- How the investigation is carried out is important.

- How findings are shared is important.

- How reports are shared is important.

- How the organisation uses the report later may decide if the privilege continues.

Often, the best protection isn’t a privilege.

The best way to protect yourself is by carrying out investigations that are:

- procedurally fair

- impartial

- based on evidence

- properly documented; and

- capable of withstanding external scrutiny

The main lesson from the Commission, the Federal Court, and oversight authorities is still the same.

In 2026, organisations that still do not understand legal professional privilege may find out too late that their supposedly confidential investigation materials can be revealed during lawsuits or regulatory checks.

Are your policies putting you at risk?

by Mick Symons

Your Policies Might Be Putting You at Risk

Many organisations highlight their policy library as evidence of effective governance oversight. After reviewing thousands of investigations, audits, and compliance failures, one fact remains unequivocally clear:

An ignored policy can create greater risk than having no policy at all.

Across Australia, organisations are increasingly facing this challenge through employee complaints, regulatory scrutiny, Ombudsman inquiries, integrity investigations, and costly litigation. The pattern remains consistent: the policy is established, yet the practice is not implemented.

The discrepancy between documented policies and actual practices now constitutes one of the most significant governance risks confronting employers.

This is precisely where ACCA provides help.

The Hidden Risk Inside Your Policy Library

Most organisations cannot answer three basic questions:

- When were your policies last reviewed?

- Do your staff members understand these?

- Could you provide evidence that they are being followed?

If the response to these questions is unclear, your organisation may be at risk.

Outdated Policies Create Legal and Regulatory Exposure

Legislation changes. Case law evolves. Regulators raise expectations.

However, many organisations continue to rely on policies that were written five, seven, or even ten years ago. A bullying policy developed before implementing psychosocial risk obligations, or a sexual harassment policy established before positive duty reforms, is outdated and is a potential liability.

Untrained staff Cannot comply with rules they do not understand

In investigations, employees regularly state:

- “I think I saw it when I started.”

- “I know we have one, but I’ve never read it.”

- “I didn’t know that was required.”

Courts and regulators routinely assess whether employees received training, whether policies were readily accessible, and whether expectations were consistently reinforced. A policy that lacks clarity and understanding is indefensible.

Managers who ignore policies create evidence against the Organisation

This is the most severe failure.

When managers circumvent procurement regulations, disregard grievance procedures, neglect to get conflict of interest declarations, or delay investigations, they generate a paper trail that compromises the organisation’s defence.

Courts evaluate actions rather than assurances.

A carefully drafted policy that is not followed may strengthen a claim against your organisation.

Why Councils and Public Entities Face Even Greater Scrutiny?

Local government and public sector bodies uphold comprehensive policy frameworks, including codes of conduct, procurement protocols, conflicts of interest management, fraud control, public interest disclosures, delegations, and governance structures.

However, volume does not equate to compliance.

Integrity agencies, auditors, and investigators consistently identify discrepancies between documented requirements and actual practices. These gaps result in reputational harm, determinations of maladministration, and, in certain instances, an elevated corruption risk.

This is the point at which independent oversight becomes essential.

How ACCA Protects Your Organisation

ACCA specialises in identifying the specific risks outlined above before their development into legal, financial, or reputational issues.

We offer independent, expert compliance support through:

Policy Health Checks

Thoroughly evaluate your current policies to confirm they accurately reflect:

- current legislation

- recent case law

- regulator expectations

- contemporary workplace risks

We identify gaps, inconsistencies, and outdated content and deliver clear, actionable recommendations.

Compliance Audits

We assess the extent to which your policies are being implemented. This encompasses:

- reviewing real‑world practices

- interviewing staff

- assessing training and awareness

- examining documentation and decision-making

- identifying where managers are bypassing requirements

This is the evidence that regulators seek — and the evidence that most organisations do not possess.

Practical, Targeted Training

We provide training that staff effectively comprehend and retain. No jargon. No generic slides. Clear, practical guidance specifically tailored to your risk profile.

Implementation Support

Policies only work when embedded. We help you:

- communicate expectations

- reinforce standards

- establish monitoring processes

- hold managers accountable

This transforms policies from static documents into dynamic controls.

If you have not tested your policies, you do not know your Risk

Most organisations can tell you how many policies they have. Few individuals can determine whether those policies are effective.

If your policies have not undergone independent review within the past two years, staff have not received training, or compliance has never been tested, it is important to act now.

When a regulator, investigator, or tribunal reviews your organisation, they will not be impressed by the volume of your policy library.

They will try to determine whether your staff adhere to it.

Strengthen your governance before someone else tests it

ACCA helps organisations to bridge the gap between policy and practice, thus safeguarding against preventable legal, financial, and reputational risks.

If you want to assess the effectiveness of your policies or require an independent compliance review, ACCA is available to help.

Contact ACCA today to schedule a confidential consultation regarding your policy framework and compliance risks.

Workplace Bullying Prevention Australia: Why Councils and SMEs Must Act Before Problems Escalate

by Mick Symons

Workplace Bullying Prevention Australia: Why Councils and SMEs Must Act Before Problems Escalate

Workplace bullying continues to challenge Australian organisations despite years of focus on workplace culture, employee wellbeing and compliance. Councils and small to medium-sized businesses (SMEs) regularly deal with the consequences of bullying complaints, including workplace investigations, staff turnover, workers’ compensation claims, damaged morale, and reputational harm.

Many organisations still view workplace bullying as an employee relations issue. That approach is no longer sufficient.

In 2026, regulators increasingly treat workplace bullying as a psychosocial hazard that employers must actively manage under workplace health and safety obligations. Organisations that ignore the warning signs expose themselves to significant legal, financial, and operational risks.

The reality is straightforward. Preventing workplace bullying costs far less than dealing with the fallout.

Why Workplace Bullying Matters More Than Ever

Workplace bullying affects far more than the individuals directly involved. It can undermine workplace culture, damage productivity, and create lasting impacts across entire teams.

When employees experience bullying, organisations often see:

- Increased absenteeism.

- Higher staff turnover.

- Reduced productivity.

- Lower employee engagement.

- Workplace conflict.

- Workers’ compensation claims.

- Costly workplace investigations.

For councils, the risks can be even greater. Allegations involving senior managers, executives or elected members can quickly attract media attention and erode community confidence.

For SMEs, the loss of a valued employee or a prolonged workplace dispute can significantly disrupt day-to-day operations.

What Is Workplace Bullying?

Workplace bullying occurs when a person or group repeatedly behaves unreasonably towards a worker or group of workers in a way that creates a risk to health and safety.

The key elements are repetition, unreasonable behaviour, and risk.

Bullying may involve:

- Repeated verbal abuse.

- Intimidation or aggressive behaviour.

- Persistent humiliation.

- Deliberately excluding individuals from workplace activities.

- Spreading rumours or gossip.

- Unreasonable workloads or deadlines.

- Withholding information necessary to perform duties.

- Harassment through emails, messaging applications or social media.

Although a single incident may not constitute workplace bullying, employers should never ignore inappropriate behaviour. Early intervention often prevents minor issues from developing into formal complaints or workplace investigations.

Workplace Bullying Is Now a Psychosocial Hazard

Australian workplaces have experienced a significant shift in how they manage employee wellbeing.

Employers are now expected to identify and manage psychosocial hazards with the same diligence they apply to physical hazards. Workplace bullying remains one of the most common and damaging psychosocial risks.

Unchecked bullying can contribute to:

- Anxiety and depression.

- Stress-related illness.

- Reduced workplace participation.

- Long-term psychological injury.

- Increased workers’ compensation costs.

The impact often extends beyond the affected employee. Teams experiencing unresolved conflict frequently suffer declining morale, reduced collaboration, and poorer performance.

Organisations that actively manage psychosocial risks are better positioned to create safe, productive, and compliant workplaces.

The Hidden Cost of Workplace Bullying

Many organisations underestimate the true cost of workplace bullying.

The direct expenses associated with complaints often include legal advice, investigations, and compensation claims. However, the indirect costs frequently exceed the visible financial impacts.

These costs may include:

- Internal investigations.

- Independent workplace investigations.

- Legal representation.

- Recruitment and onboarding expenses.

- Lost productivity.

- Increased sick leave.

- Reduced employee engagement.

- Damage to organisational reputation.

Every bullying complaint consumes management time and organisational resources. The longer issues remain unresolved, the more expensive they become.

Why Councils Face Unique Risks

Local government operates in an environment where transparency, accountability and public trust are essential.

Unlike private sector organisations, councils must manage workplace issues while maintaining public confidence and responding to community expectations.

Poorly managed workplace bullying complaints can result in:

- Governance reviews.

- Community criticism.

- Political pressure.

- Adverse media coverage.

- Reputational damage.

A complaint that begins as an internal employment matter can quickly become a public issue.

That reality makes early intervention and effective workplace culture management critical for councils of all sizes.

Leadership Shapes Workplace Culture

Strong leadership remains the most effective defence against workplace bullying.

Employees closely observe how leaders behave and what behaviour they tolerate. Managers who ignore inappropriate conduct often create an environment where bullying flourishes.

Leaders who consistently demonstrate professionalism, accountability and respect set a very different standard.

Effective leaders:

- Address concerns promptly.

- Communicate expectations clearly.

- Support respectful workplace behaviour.

- Hold individuals accountable.

- Promote psychological safety.

Organisations rarely regret acting too early. They often regret acting too late.

Policies Alone Will Not Prevent Bullying

Every organisation should maintain a clear workplace bullying policy. However, policies only work when employees understand them, and leaders apply them consistently.

An effective policy should:

- Define workplace bullying.

- Provide practical examples.

- Explain reporting pathways.

- Outline investigation procedures.

- Emphasise procedural fairness.

- Explain confidentiality obligations.

- Identify available support services.

A policy hidden on an intranet page will not change workplace behaviour.

Employees need confidence that leaders will enforce the policy fairly and consistently.

Training Builds Capability and Accountability

Workplace bullying prevention requires ongoing education.

Employees need to understand what bullying looks like, how to report concerns and what standards of behaviour the organisation expects.

Managers require additional skills in:

- Complaint management.

- Conflict resolution.

- Difficult conversations.

- Psychosocial risk management.

- Early intervention strategies.

- Workplace investigations.

Regular training helps organisations reinforce expectations and maintain a respectful workplace culture.

Early Intervention Prevents Escalation

Most serious workplace disputes begin with relatively minor issues that organisations fail to address.

Common warning signs include:

- Interpersonal conflict.

- Increased complaints.

- Team dysfunction.

- Employee disengagement.

- Declining morale.

- Increased absenteeism.

Managers who identify these indicators early can often resolve issues through coaching, mediation, facilitated discussions or other informal processes.

Early intervention remains one of the most effective workplace bullying prevention strategies available.

When Should You Engage an External Investigator?

Some matters require an independent assessment.

External workplace investigators may be appropriate when:

- Senior managers are involved.

- Conflicts of interest exist.

- Serious misconduct is alleged.

- Multiple parties are involved.

- Organisational impartiality may be questioned.

- Significant reputational risks exist.

An independent investigation helps demonstrate procedural fairness, transparency, and objectivity.

For councils, government agencies and larger SMEs, independent investigations often provide confidence to employees, executives, governing bodies, and the wider community.

Creating a Respectful Workplace Culture

Preventing workplace bullying requires more than policies, training sessions and investigations.

It requires leadership commitment and a workplace culture built on respect, accountability, and professionalism.

Organisations that encourage employees to raise concerns early, address complaints fairly and support respectful behaviour create safer and more productive workplaces.

The benefits are substantial:

- Stronger employee engagement.

- Higher retention rates.

- Better organisational performance.

- Reduced workplace conflict.

- Lower legal and compliance risks.

Final Thoughts

Workplace bullying is no longer simply an HR issue. It is a workplace health and safety issue, a governance issue, and a leadership issue.

Councils and SMEs that invest in workplace bullying prevention, psychosocial risk management, leadership development and workplace culture create stronger, safer, and more resilient organisations.

Those that delay action often face escalating conflict, costly investigations, reduced productivity, and reputational damage.

The most successful organisations understand a simple truth: preventing workplace bullying is not just about compliance. It is about protecting people, strengthening culture, and building a workplace where employees can perform at their best.

Is Legal Professional Privilege Still Relevant for Workplace Investigations in 2026?

by Mick Symons

Update June 2026: This article has been expanded to include recent Federal Court commentary, additional case studies and practical guidance for councils, government agencies and SMEs. Read our updated article: “Is Legal Professional Privilege Still Relevant for Workplace Investigations in 2026?“

Is Legal Professional Privilege Still Relevant for Workplace Investigations in 2026?

Many councils, government agencies, and employers still believe that hiring lawyers to carry out a workplace investigation automatically protects the process with legal professional privilege.

That idea is still risky.

Australian courts and tribunals keep confirming that simply having a law firm involved does not create privilege. The crucial question is whether the investigation is mainly to get legal advice or to get ready for a lawsuit.

By 2026, this problem has become more important because investigations now more often include:

- psychological and social risks

- accusations of bullying and harassment

- complaints about unwanted sexual behaviour

- reporting of wrongdoing by an insider

- code of Conduct breaches

- conflicts of interest

- fraud and corruption allegations

- unfair dismissal proceedings; and

- workers’ compensation and workplace conflicts

Employers who do not understand privilege may accidentally reveal sensitive information during lawsuits, Commission hearings, court reviews, and investigations.

The Key Legal Principle

The High Court’s decision in Esso Australia Resources Ltd v Commissioner of Taxation (1999) 201 CLR 49 is still the fundamental rule. Privilege applies only when the main reason for the communication or document is to get or give legal advice, or to use it in current or expected legal cases.

Who the investigator is does not matter.

If the primary goal of the investigation is to find out if rules were broken, if bad behaviour happened, or if someone should be disciplined, then privilege might not protect the information.

The Fair Work Commission Warning Employers Still Ignore

One of the most important workplace investigation decisions is Gaynor King [2018] FWC 6006.

The City of Darwin hired Minter Ellison to look into bullying claims. The Council later said the report was confidential because lawyers carried out the investigation.

Commissioner Wilson did not accept that argument.

The Commission looked into the real reason for the investigation and found that the main goal was to see if workplace behaviour rules and Council policies were broken, not to get legal advice.

The Commission also looked at how the employer acted: employees were told about the investigation, the accusations, and the results. Sharing this information weakened the claim of privilege.

That decision is still very important in 2026 because many organisations still organise investigations in ways that do not protect privilege.

Why Some Investigation Reports Remain Protected

Privilege applies when the investigation is done mainly to get legal advice.

In the cases Bowker, Coombe and Zwarts v DP World Melbourne Ltd [2015] FWC 7312 and Kirkman v DP World Melbourne Ltd [2016] FWC 605, the Fair Work Commission agreed that certain information was protected because the investigators were hired specifically to help lawyers give legal advice.

The Commission examined:

- the exact words used in the retainer

- the role of the lawyers

- the reason for the investigation

- how documents were managed

- whether findings were broadly disclosed; and

- whether the employer kept things confidential as they should

Privilege is determined by how things are organised, their goals, and how people behave—not by job titles or guesses.

Recent Federal Court Commentary (2023–2026)

The Federal Court’s decision in Diawara v National Australia Bank Limited [2023] FCA 1048 provides one of the most important recent clarifications. (Australasian Lawyer)

The case was about a claim of privilege over a cultural review report created during a discrimination dispute. The Court confirmed that:

- the dominant purpose test remains the central inquiry

- the focus is on why the person made or obtained the document

- the party claiming privilege must prove the necessary facts; and

- privilege can apply even if the document is used for secondary or additional purposes

The Court looked at the agreement between Herbert Smith Freehills and Wise Workplace Solutions and agreed that the main reason for the report was to help the lawyers legally advise NAB.

This decision confirms that privilege can be kept, but only when the evidence clearly shows that the main reason was legal advice.

Recent Oversight Commentary

A 2022 external review by the South Australian Ombudsman highlighted the importance of the dominant purpose test when evaluating claims of privilege over investigation materials. The Ombudsman said that if investigations mainly focus on gathering facts about employee complaints or policy violations, claims of privilege might fail unless the evidence clearly shows the investigation was for obtaining legal advice.

The Ombudsman also emphasised that labelling a document “privileged and confidential” does not make it privileged. Courts and oversight agencies will focus on the true nature of the work and the actual reason for the investigation.

Why This Matters for Local Government

The problem is especially serious for councils.

Local government investigations often include:

- councillor behaviour

- allegations against a senior executive

- code of Conduct matters

- complaints about bullying

- procurement concerns

- allegations of corruption

- protected disclosures; and

- conflicts of interest

Many councils believe that hiring outside lawyers guarantees privacy.

That assumption becomes a problem when things get to:

- The Fair Work Commission

- NCAT

- ICAC

- The NSW Ombudsman

- Legal process

- Public interest disclosure investigations; or

- Judicial review.

If privilege doesn’t apply, sensitive information might be exposed, including:

- draft findings;

- internal communications;

- witness credibility assessments;

- legal assumptions;

- procedural weaknesses; and

- governance failures.

The Practical Lessons for Employers in 2026

Organisations should not automatically assume they have special rights just because lawyers are investigating.

The safer approach is to separate:

- factual investigations

- disciplinary decision-making

- witness evidence collection; and

- legal advice.

Employers should get advice early on how to organise the investigation before choosing investigators.

- Retainer documents are important.

- How the investigation is carried out is important.

- How findings are shared is important.

- How reports are shared is important.

- How the organisation uses the report later may decide if the privilege continues.

Often, the best protection isn’t a privilege.

The best way to protect yourself is by carrying out investigations that are:

- procedurally fair

- impartial

- based on evidence

- properly documented; and

- capable of withstanding external scrutiny

The main lesson from the Commission, the Federal Court, and oversight authorities is still the same.

In 2026, organisations that still do not understand legal professional privilege may find out too late that their supposedly confidential investigation materials can be revealed during lawsuits or regulatory checks.

Governance Matters — Especially When Nobody Is Watching

by Mick Symons

Governance Matters — Especially When Nobody Is Watching

Governance Looks Strong on Paper — But Is It?

Today, most organizations publicly champion governance, compliance, and accountability.

They publish policies, codes of conduct, procurement procedures, fraud control frameworks, workplace behaviour standards, and risk management plans. Boards and executive teams routinely tackle integrity, transparency, and compliance obligations.

Despite these efforts, governance failures persist across Australia.

By 2026, policies are rarely the problem. The problem is whether those policies are truly understood, consistently applied, properly enforced, and backed by leadership behaviour.

Many organizations seem compliant outwardly, while serious problems silently brew beneath.

This remains a top governance risk for councils, government agencies, and SMEs.

Why Governance Failures Still Occur in 2026

Modern organizations navigate ever-tougher environments.

Councils and government departments confront:

- rising community expectations

- tighter financial pressures

- increasing regulatory obligations

- workforce shortages

- cyber security threats

- procurement scrutiny

- heightened public accountability

SMEs face these common challenges:

- rising operating costs

- staffing pressures

- economic uncertainty

- increasing compliance obligations

- intense commercial competition

Under pressure, organizations can slowly normalize poor practices.

Shortcuts may replace proper processes. Oversight can weaken. Employees may avoid reporting concerns out of fear of conflict, reputational damage, or career repercussions.

Importantly, governance failures seldom start with major misconduct.

They often start with small rationalizations:

- “we need to get this project finished.”

- “everyone does it this way.”

- “it’s only temporary.”

- “the organization cannot afford delays.”

Repeated compromises eventually erode accountability, transparency, and organizational integrity.

Performance Pressure and Ethical Risk

A top governance risk in 2026 is performance pressure.

Many organizations intensely focus on:

- financial performance

- project delivery

- operational targets

- KPIs

- political expectations

- public image

While performance matters, problems arise when organizations prioritize outcomes over ethical decisions and proper oversight.

This can foster environments where employees feel pressured to:

- manipulate reporting

- ignore compliance failures

- bypass procurement controls

- avoid documenting concerns

- conceal mistakes

- protect reputations instead of addressing problems

In many investigations, warning signs appeared well before formal action.

The failure was not because of lack of information. The failure was the unwillingness to confront the problem early.

Why Councils and SMEs Remain Vulnerable

Local Government Risks

The failure was the unwillingness to confront the problem early.

- public funds

- procurement processes

- development approvals

- community services

- infrastructure projects

- regulatory functions

Even the perception of favoritism, poor transparency, weak procurement controls, or inconsistent decisions can erode community confidence.

Public trust is hard to earn and easy to lose.

Poor governance also exposes councils to:

- reputational damage

- regulatory scrutiny

- legal disputes

- workplace conflict

- adverse media attention

- loss of community confidence

SME Risks

SMEs face distinct yet equally serious governance challenges.

Smaller organizations often depend on trusted staff, informal systems, and minimal oversight.

Without strong internal controls, businesses risk becoming vulnerable to:

- procurement manipulation

- payroll irregularities

- fraud

- conflicts of interest

- financial misconduct

- cyber-related scams

- poor record keeping

In many SMEs, governance weaknesses are not deliberate. They develop gradually because operational pressures take priority over oversight.

Warning Signs Leaders Often Ignore

They develop gradually as operational pressures overshadow oversight.

Common indicators include:

- resistance to scrutiny

- poor record keeping

- inconsistent decision-making

- weak procurement controls

- lack of policy enforcement

- repeated complaints about transparency

- employees afraid to report concerns

- senior staff avoiding accountability

- excessive reliance on one employee controlling key functions

- unexplained financial anomalies

- informal approval processes

- poor complaint handling

Organizations must take these indicators seriously.

Unaddressed small issues can escalate into major organizational, financial, and reputational risks.

Governance Is More Than Compliance

Strong governance isn’t about the number of policies an organization has.

It is measured by:

- leadership behaviour

- accountability

- transparency

- ethical decision-making

- effective oversight

- consistent policy enforcement

- willingness to address misconduct

- organizational culture

Policies alone don’t build integrity. Leadership behaviour does.

Leadership behaviour delivers.

When leaders dodge tough talks, skip consistent standards, or put reputation over accountability, organizational culture can quickly decay.

Building a Culture of Accountability

Organizations that manage governance risks effectively share key characteristics.

They:

- encourage reporting of concerns

- respond to complaints consistently

- maintain strong procurement and financial controls

- review policies regularly

- provide ongoing staff training

- support independent oversight

- act early when warning signs emerge

- prioritize transparency and accountability

Strong organizations know governance is not a onetime exercise.

Governance demands constant focus, regular review, and strong leadership commitment.

Final Thoughts

Governance failures continue to harm councils, government agencies, and SMEs across Australia.

The lesson is obvious.

A policy on a shelf offers little protection without a culture of integrity, accountability, transparency, and ethical leadership.

Real governance is not about appearances.

It is about what leaders, managers, and employees do when no one’s watching.

Contact [email protected] for help in these areas.

How Should Employers Address Misconduct Allegations in 2026?

by Mick Symons

How Should Employers Address Misconduct Allegations in 2026?

Allegations of workplace misconduct are becoming more complicated, more noticeable, and much more dangerous for employers in 2026.

Local councils, government agencies, and small businesses are now receiving more complaints about:

- bullying and harassment

- conflicts of interest

- misuse of resources

- fraud and corruption

- inappropriate social media conduct

- discrimination

- workplace behavioural issues

Meanwhile, employees now have vastly different expectations. Employees better understand their workplace rights, psychological safety requirements are being examined more closely, and organisations face increasing demands to show fairness, transparency, and accountability.

A single investigation that is not managed well can rapidly become more serious:

- unfair dismissal proceedings

- workers compensation claims

- psychological injury allegations

- reputational damage

- union disputes

- media scrutiny

- loss of staff confidence

Despite these changing risks, one principle stays the same:

Procedural fairness remains central to every justifiable workplace investigation.

Why Procedural Fairness Still Matters

Procedural fairness is not just an HR formality or a legal technicality.

It supports a legal and trustworthy investigation process.

Employees who face allegations must be provided with:

- clear details of the allegations

- enough time to respond

- access to relevant information

- an opportunity to provide evidence

- a fair and unbiased assessment process

Investigators and decision-makers should remain open-minded throughout the entire investigation. If an investigator works backward from a desired result, the honesty of the process is already affected.

The Fair Work Commission keeps emphasising that assumptions, hints, and unsupported opinions cannot replace factual evidence.

The Continuing Relevance of Deng v Westpac

One of the most often talked about cases about procedural fairness is Kefeng Deng v Westpac Banking Corporation [2018] FWC 7334. (CaseNote)

Westpac looked into claims about using customer information improperly and breaking internal rules. Although the Commission agreed that there were valid concerns about the employee’s behaviour, the investigation process itself faced strong criticism.

The Fair Work Commission pointed out several major failures, including:

- insufficient detail provided before the interview

- a five-hour interview with minimal breaks

- failure to thoroughly test or corroborate evidence

- an apparent overreliance on the investigator’s opinion

- only 24 hours provided for the employee to respond to detailed allegations

Commissioner Riordan said parts of the process were unfair and criticised the investigation for not properly following important leads. The Commission ultimately determined that the dismissal was unfair and ordered the employee to be reinstated.

The decision is still especially important in 2026 because many organisations keep making the same mistakes.

Common Investigation Failures Still Seen in 2026

Although people are more aware of governance and workplace culture, many employers still do not fully understand how complex misconduct investigations can be.

Frequent problems include:

- managers investigating their own staff without training

- poorly framed allegations

- lack of independence

- rushing investigations

- failing to gather corroborating evidence

- excessive delays

- inadequate interview practices

- confidentiality breaches

- failing to separate fact from opinion

- predetermined outcomes

In local government settings, these problems become more serious because investigations often draw political attention, council members’ examination, and public interest.

For SMEs, the impact can be equally damaging. An investigation with mistakes can damage workplace relationships, lower morale, and cause long-term harm to reputation.

Why Poor Investigations Create Bigger Problems

Many organisations strongly emphasize “resolving the issue quickly.”

This approach often leads to much higher risks in the long term.

An investigation conducted poorly can be detrimental:

- complainants

- respondents

- witnesses

- workplace culture

- leadership credibility

- staff trust

- public confidence

Employees soon lose trust in systems they see as biased, inconsistent, or unfair.

When trust is lost, organisations often experience more complaints, higher employee turnover, and employees becoming less willing to report wrongdoing.

What a Professional Investigation Looks Like in 2026

A proper workplace investigation should include:

- logical terms of reference

- properly articulated allegations

- impartial investigators

- evidence-based findings

- procedural fairness throughout

- documented reasoning

- proportionate recommendations

- independent review of findings before disciplinary action

Importantly, findings must always rely on evidence rather than assumptions, office politics, or the pressure to reach a quick result.

Effective investigations follow a systematic and fair approach and can withstand careful examination by others.

The Value of Independent Investigators

For important, sensitive, or high-risk issues, independent investigators offer some of the best protections for councils, government agencies, and small and medium-sized enterprises.

Independent investigators provide:

- objectivity

- investigative expertise

- procedural fairness experience

- evidentiary assessment skills

- independence from internal politics

- increased credibility

External investigators also help show employees, regulators, and tribunals that the organisation handled the matter fairly and professionally.

That trustworthiness can become especially important if the issue later goes to the Fair Work Commission, a regulator, or the media.

Final Thoughts

By 2026, workplace investigations must be handled with greater seriousness than just routine HR tasks.

Allegations of misconduct now have major legal, operational, cultural, and reputational affects.

The organisations best able to handle these risks are those that:

- act early

- investigate professionally

- maintain procedural fairness

- document decisions carefully

- remain evidence-focused throughout the process

When investigations are conducted correctly, organisations protect both themselves and the integrity of their workplace culture.

Interviewing Elderly Witnesses and Victims: Best Practice for Fraud, Elder Abuse and Workplace Investigations

by Mick Symons

Interviewing Elderly Witnesses and Victims: Best Practice for Fraud, Elder Abuse and Workplace Investigations

Investigators handling fraud, elder abuse and workplace matters need interview methods that protect evidence, reduce risk and respond appropriately to the communication, cognitive and trauma-related needs that may affect older witnesses and victims.

Why Older Interviewees Require a Different Investigative Approach

As Australia’s population ages, investigators are increasingly required to interview elderly people as witnesses and as victims. These interviews arise across a wide range of matters — including fraud, elder abuse, family violence, institutional misconduct, workplace investigations, insurance claims, and serious criminal offences.

Yet many investigations still apply one-size-fits-all interviewing techniques that fail to account for age-related vulnerabilities. When this happens, the consequences can be significant: unreliable evidence, distressed interviewees, and investigations that fail under legal scrutiny.

This article examines best practice for interviewing elderly witnesses and victims, outlines key safeguards, and highlights why poor interviewing — not age — is often the real source of evidentiary problems.

Why Interviewing Elderly People Requires Careful Adjustment

Age alone does not determine a person’s reliability or credibility. Many older people provide clear, accurate and detailed accounts. However, investigators must recognise that ageing can be associated with changes that affect the interview process, including:

- hearing or vision impairment

- reduced stamina or fatigue

- medication effects

- slower processing speed

- mild cognitive impairment or dementia

- heightened anxiety, particularly in formal settings

Importantly, these factors affect how information is communicated, not necessarily whether the information is true.

When investigators fail to adapt their approach, inconsistencies may be introduced that are later (incorrectly) attributed to the witness’s age.

Elderly Victims vs Elderly Witnesses: Is There a Difference?

There is overlap in approach, but the context and risks differ.

Elderly victims

Elderly victims may be dealing with:

- trauma (recent or historic),

- dependency on carers or family members,

- fear of retaliation or loss of support,

- shame or reluctance to report abuse.

Common examples include financial exploitation, neglect, family violence, or institutional abuse.

Elderly witnesses

Elderly witnesses may not be personally harmed but may:

- feel pressure due to formal legal processes,

- worry about “getting it wrong”,

- experience stress when questioned aggressively,

- disengage if treated dismissively.

In both cases, rapport, respect, and structure are essential.

Preparing for the Interview: Setting the Conditions for Success

Choose the right environment

The interview setting matters more than many investigators realise. Best practice includes:

- a quiet room with minimal background noise

- good lighting without glare

- seating that allows face-to-face conversation at eye level

- space for mobility aids

- removal of physical barriers such as large desks

Where appropriate, conducting the interview in a familiar location (such as the person’s home or a community facility) may improve comfort and recall.

Timing matters

Older adults may experience:

- fatigue later in the day,

- medication cycles that affect concentration,

- reduced tolerance for long interviews.

Investigators should:

- ask when the person feels most alert,

- plan shorter sessions with breaks,

- be open to multiple interviews if required.

Conducting the Interview: What Works (and What Doesn’t)

Start with rapport, not questions

Many older people feel dismissed or rushed by professionals. Taking time to:

- introduce yourself clearly,

- explain your role and purpose,

- outline what will happen next,

can significantly improve cooperation and recall.

A calm, respectful tone is not “soft” — it is forensically effective.

Use open-ended, non-suggestive questions

As with child forensic interviewing, research consistently shows that open narrative produces the most reliable information.

Effective examples include:

- “Can you tell me, in your own words, what happened?”

- “What do you remember about that day?”

- “You mentioned X — can you tell me more about that?”

Avoid:

- rapid-fire questioning,

- interrupting narratives,

- multi-part questions,

- leading or assumptive language.

When clarification is required, phrases such as “Help me understand…” are preferable to confrontation.

One idea per question

Cognitive load matters. Questions that bundle multiple concepts (“Where were you, who was with you, and what time was it?”) can overwhelm and confuse.

Instead:

- ask one question at a time,

- pause and allow processing time,

- check understanding without patronising.

Safeguards When Cognitive Impairment Is Present

Some elderly interviewees may have mild cognitive impairment or dementia. This does not automatically render their evidence unreliable, but it does require additional safeguards.

Best practice includes:

- shorter interviews,

- simpler sentence structure,

- frequent breaks,

- avoiding hypothetical questions,

- confirming understanding gently.

Where capacity is genuinely in doubt, investigators must consider legal and ethical obligations around consent and representation.

Trauma-Informed Interviewing with Elderly Victims

Many elderly victims have experienced cumulative trauma across their lives. A trauma-informed approach recognises that:

- memory may be fragmented,

- emotional responses may appear delayed or muted,

- minimisation is common (“It wasn’t that bad”).

Investigators should avoid interpreting these responses as dishonesty. Courts and inquiries — including findings of the Royal Commission into Institutional Responses to Child Sexual Abuse — have repeatedly highlighted how interviewing style can distort evidence.

Lessons from Courts and Public Inquiries

Judicial criticism frequently focuses not on what an elderly person remembered, but how they were questioned.

Common themes include:

- excessive pressure on vulnerable witnesses,

- confusing or misleading questions,

- failure to accommodate impairment,

- dismissive treatment affecting credibility.

Australian courts have increasingly emphasised the need for procedural fairness and appropriate safeguards for vulnerable witnesses, including older adults.

Applying These Principles in Fraud, Elder Abuse and Workplace Investigations